When I approached Ed Murray about writing a guest post for his site, I knew I wanted to intertwine both of our areas of expertise. His in writing and literature and mine in personal finance. I also knew it needed to be truly valuable if it were to grace the pages of his site. (For some reason, he rejected my first guest post, “How to Make Money the Old-Fashioned Way: Bank Robbery”.)

In fact, reading Ed’s articles and the books he has published inspired me to launch my own website this past summer, The Sensible Merchant, where I try to bridge the gap between personal finance and mental health, as well as the technology trends that are beneficial to both. I relied heavily on the tips and guidance that Ed has posted over the years to launch my site.

This idea of passing along knowledge to help others get to where you are is so inspiring to me. That’s why when I started seeing Ed’s posts about how to write better, how to read more, and how to avoid blogging mistakes, I knew that I wanted to join in on the project.

The fact that this type of content can be ad-supported or that referrals can help the authors financially means that there’s less incentive to paywall it and a greater chance for it to spread and help others. I believe that this information sharing engine propels itself upwards and contributes to the collective betterment of our society as a whole.

On to the reason for my post…

Investing is simply making more money by using your existing money. But if you don’t have any money to invest to begin with, you’ll constantly be on the treadmill of living paycheck to paycheck, working well past your desired retirement age, and being unable to provide for your future self and your future family.

Worse, yet, is the fact that until you know how to prioritize saving, any number of emergencies may push you so deep into debt that your future prospects of accumulating wealth may be non-existent.

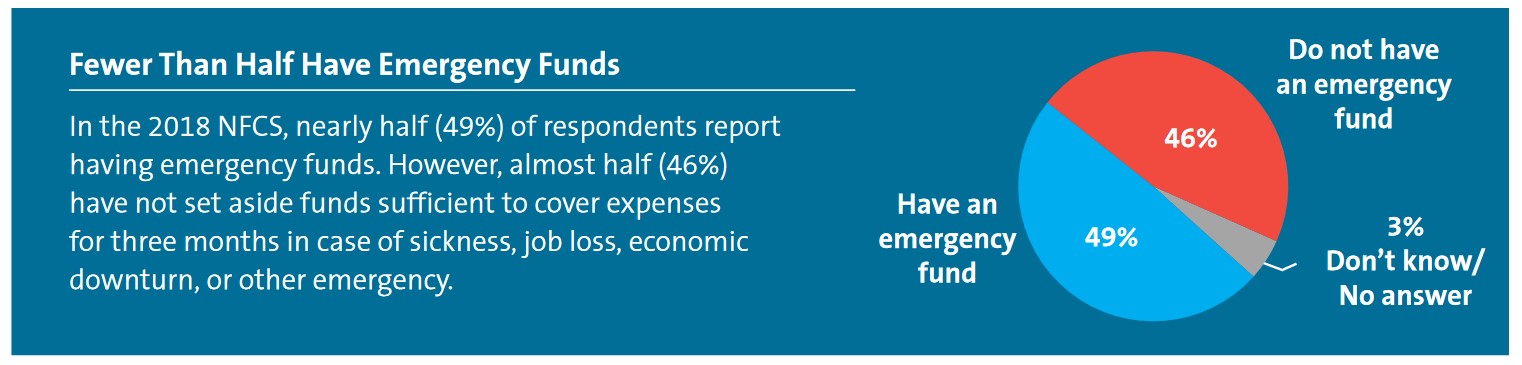

This is why personal finance education strikes me as universally necessary and especially applicable during a time in U.S. history that has seen wealth inequality growing at incredible rates. Many people don’t even know there is a financial freedom path they can begin to walk down, no matter their age or level of knowledge. The data below shows that this was an issue prior to the COVID-19 pandemic:

The differences have only become more stark as the 2020 pandemic continues, where the poorest and most at-risk individuals have been completely left behind financially due to an exogenous event outside of their control.

I know there are myriad factors that contribute to this issue, and I try to explore them from time to time on my site, but I overwhelmingly believe that a little bit of education in personal finance a little bit earlier in life goes a long way. Personal finance education can and should be free, accessible, and practical at whatever income bracket you happen to find yourself in.

To that end, I want to pass along a few recommendations: 1) a website for beginners, 2) a book for experienced investors, and 3) a podcast for everyone.

Website Recommendation: Get Rich Slowly

Get Rich Slowly is one of the most accessible and practical personal finance sites out there. This website is responsible for me opening up my own Roth IRA back when I was in my early twenties. Giving me that motivation alone would be worth its weight in gold (or stocks in this case), but since then the site has evolved and become really streamlined for folks who are brand new to managing and growing their own finances.

The author, J.D. Roth, takes a holistic approach to money management and often points out how other areas of your life will factor into your finances. That’s why I love this site so much and try to capture similar ideals and topics on my own site.

For example, most people universally want to be rich, but how do you know when you’re rich? Is it a dollar amount? Is it the square footage of your home? Of course not. This article discusses the sweet spot between a fulfilling life and the amount in your bank account.

Book Recommendation: The Little Book of Market Myths

I’ve read a lot of books about psychology, history, and finance over the years, and this book does the best job of them all at debunking many of the common misconceptions that most people accept as truth about money and how to make more of it.

Ken Fisher and Lara Hoffmans use data, common sense, and simple terminology to give readers a view into the world as seen through one of the most successful investors of all times (Ken Fisher is the founder of Fisher Investments, a well-known financial advisory firm).

For example, most people think high-unemployment is bad for stocks. They want to wait until the economy is firing on all cylinders and everyone has a job until they invest their hard-earned money in a volatile stock market. But this is precisely the type of thinking that ensures you will enter the market too late to see the biggest returns. Ken spends an entire chapter discussing how unemployment, the private sector, and the stock market are related.

Podcast Recommendation: Animal Spirits

Maybe you like to consume your content on the go. In that case, I’d like to recommend my favorite financial podcast: Animal Spirits.

I was initially persuaded to listen to this podcast by a Certified Financial Planner. That means these are the investment advisors that your investment advisors listen to. But they don’t over complicate things. They stay current, non-political, and have excellent and witty banter on a range of topics.

Another reason this is my go-to finance podcast is that both of these guys author and update their own financial blogs regularly. I recommend that if you enjoy their show, you also subscribe to their newsletters:

Finally, and most importantly, they will tell you when they don’t know something or are working on a theory. In a world where everyone wants to be an expert, it’s refreshing to hear an actual expert admit when they’ve been wrong or don’t know the answer. This helps others (like me) learn from their mistakes. Full transparency is key to credibility and they earn it.

The Takeaway

While these recommendations are geared towards learning more about finances in general, the last recommendation I want to make is that you start viewing finances as being affected by the quality of your life, not the other way around. And the quality of your life is affected by the quality of your mind. This is why reading profusely is so important. This is why introspection is so important. It’s why I try to weave basic personal finance together with advocating for an awareness of our own mental health.

Not all dollars spent are spent equally. We can only pay attention to so many things throughout the day. By being extra aware of our values, and spending less on the frivolous or fleeting items that are marketed to us, we have more available to invest back into ourselves. The real value of money isn’t in getting a nicer car or going on a bigger vacation than last year. It’s in using it to acquire more time and then spending that time in more and more effective and fulfilling ways for yourself and those around you.

As founder and author of The Sensible Merchant, Kevin Hall researches the personal finance industry, the world of mental health, and technology trends to educate readers on these topics… albeit poorly. Visit The Sensible Merchant for more!

What do you think?